A View From The Tower - 4th Quarter 2024

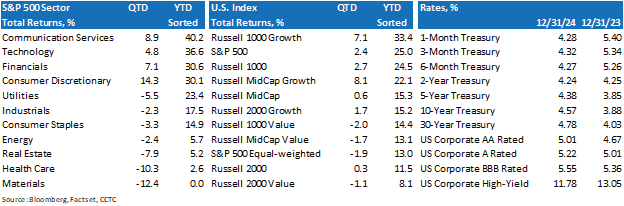

In 2024, U.S. large-cap equities, those companies whose equity is valued at $10 billion or greater, experienced a second year of growth, with the S&P 500 rising 25% (its second consecutive year of 20%+ performance, for the first time since the 1990’s) and the Nasdaq Composite gaining nearly 30%. The surge was fueled by a robust economic backdrop, earnings growth, moderating inflation, and the Federal Reserve’s interest rate cuts. The “Magnificent 7” tech stocks (Microsoft, Amazon, Meta, Apple, Alphabet, Nvidia, Tesla) significantly contributed to these gains, showcasing the dominance of large-cap growth companies. Despite some volatility, especially in the latter part of the year, investor optimism surrounding artificial intelligence and a favorable economic environment helped maintain momentum.

The Current Expansion Seems to Be Quite Stable

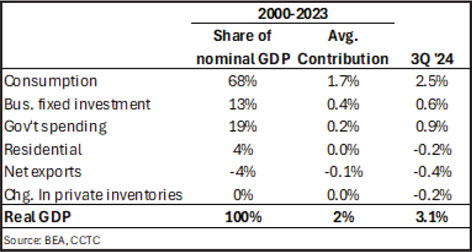

Year-over-year GDP likely expanded by approximately 2.5% in 2024, above estimated trend growth of about 2%. Consumption has benefitted from 20 straight months of year-over-year real wage gains, 48 consecutive months of job gains and an estimated $26 trillion in net worth created over the past two years. Business fixed investment has also contributed to growth. We believe strong corporate profits (consensus estimates for earnings growth for the S&P 500 in 2025 are near 15%) and artificial intelligence enthusiasm should continue to encourage growth in business investment. Another driver of business investment, although somewhat less predictable, is legislation to promote domestic production of goods, such as the CHIPS act. This bill provided $53 billion in funding to bolster U.S. semiconductor capacity and increase production in technology related industries. With consumption and business investment accounting for 81% of GDP and continuing to grow steadily, we could see 2025 GDP growth approximating that of 2024. Obviously, the consumer could play the most important role in 2025 growth. There are a few wrinkles, as there always are, but in general we think the consumer looks healthy.

Year-over-year GDP likely expanded by approximately 2.5% in 2024, above estimated trend growth of about 2%. Consumption has benefitted from 20 straight months of year-over-year real wage gains, 48 consecutive months of job gains and an estimated $26 trillion in net worth created over the past two years. Business fixed investment has also contributed to growth. We believe strong corporate profits (consensus estimates for earnings growth for the S&P 500 in 2025 are near 15%) and artificial intelligence enthusiasm should continue to encourage growth in business investment. Another driver of business investment, although somewhat less predictable, is legislation to promote domestic production of goods, such as the CHIPS act. This bill provided $53 billion in funding to bolster U.S. semiconductor capacity and increase production in technology related industries. With consumption and business investment accounting for 81% of GDP and continuing to grow steadily, we could see 2025 GDP growth approximating that of 2024. Obviously, the consumer could play the most important role in 2025 growth. There are a few wrinkles, as there always are, but in general we think the consumer looks healthy.

As Usual, Consumers Are driving the Boat

Consumers play a pivotal role in the U.S. economy. Their spending accounts for around 70% of the gross domestic product (GDP), which means that the economic health of the nation is heavily reliant on consumer behavior. When consumers are confident and spend more, businesses thrive, leading to job creation and economic growth. Conversely, when consumer spending declines, it can lead to economic slowdowns or recessions.

Consumers play a pivotal role in the U.S. economy. Their spending accounts for around 70% of the gross domestic product (GDP), which means that the economic health of the nation is heavily reliant on consumer behavior. When consumers are confident and spend more, businesses thrive, leading to job creation and economic growth. Conversely, when consumer spending declines, it can lead to economic slowdowns or recessions.

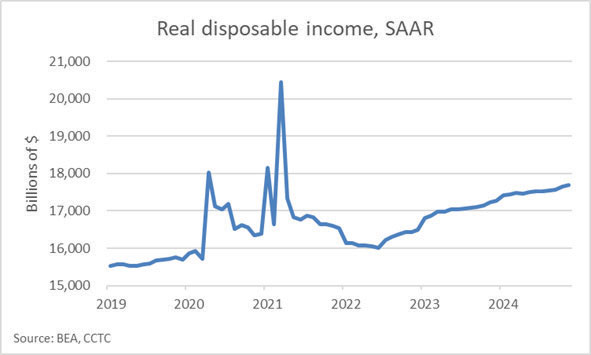

Real disposable personal income (RDPI) is one of the more important indicators when judging the health of the U.S. economy. RDPI represents the amount of income individuals have after paying taxes and adjusting for inflation. It reflects the true spending power of consumers, as  it accounts for changes in the cost of living. When RDPI increases, consumers generally have more money to spend on goods and services, which can boost overall economic activity. Also, an increase in RDPI indicates that people have more financial flexibility and can afford to save, invest, and spend on discretionary items. Although inflation has been a top concern for a few years, the consumer has increased its capacity to spend. RDPI is up 14% since the beginning of 2019. We look for the upward trend to carry on, as additional jobs are created and progress on the inflation front continues to help increase real earnings.

it accounts for changes in the cost of living. When RDPI increases, consumers generally have more money to spend on goods and services, which can boost overall economic activity. Also, an increase in RDPI indicates that people have more financial flexibility and can afford to save, invest, and spend on discretionary items. Although inflation has been a top concern for a few years, the consumer has increased its capacity to spend. RDPI is up 14% since the beginning of 2019. We look for the upward trend to carry on, as additional jobs are created and progress on the inflation front continues to help increase real earnings.

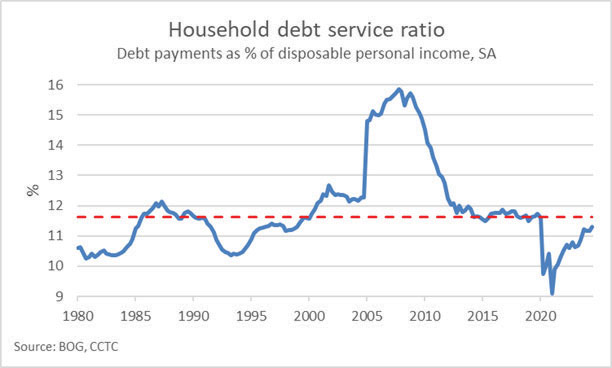

The Household Debt Service Ratio (HDR) also shows that the consumer remains relatively healthy. The HDR is a metric that measures the proportion of disposable personal income that households allocate to servicing their debt obligations. It includes payments on mortgages and consumer debt such as credit cards, auto loans, and student loans. The current DSR of 11.3% remains slightly below its pre-pandemic trend and its longer-term median of 11.6%. This suggests that consumers are not overburdened with debt payments and should allow future spending increases on par with income growth.

The Household Debt Service Ratio (HDR) also shows that the consumer remains relatively healthy. The HDR is a metric that measures the proportion of disposable personal income that households allocate to servicing their debt obligations. It includes payments on mortgages and consumer debt such as credit cards, auto loans, and student loans. The current DSR of 11.3% remains slightly below its pre-pandemic trend and its longer-term median of 11.6%. This suggests that consumers are not overburdened with debt payments and should allow future spending increases on par with income growth.

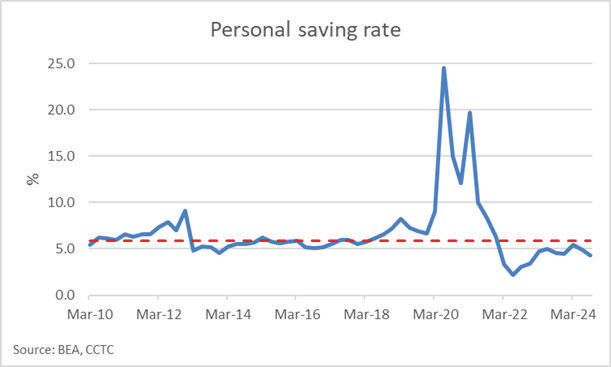

The personal savings rate (PSR) is the percentage of disposable personal income that individuals save rather than

The personal savings rate (PSR) is the percentage of disposable personal income that individuals save rather than

spend. Levels of the PSR can give us valuable information about consumer confidence and beliefs about the future direction of the economy. A high savings rate suggests that consumers are cautious about the future and are prioritizing saving over spending. A low saving rate could indicate that consumers are confident about future economic growth. This can boost economic growth as increased consumer spending drives demand for goods and services. Prior to 2020, the savings rate generally hovered around historically low levels. Economic growth and a robust job market encouraged spending. During the pandemic, savings surged, thanks to lockdowns, reduced spending opportunities, and government stimulus packages. However, PSR’s cannot be viewed in a vacuum. For example, lower savings rates during a period of high inflation may be viewed as consumers struggling to cover expenses given current income and saving less. This last point is currently a concern, especially for lower income consumers.

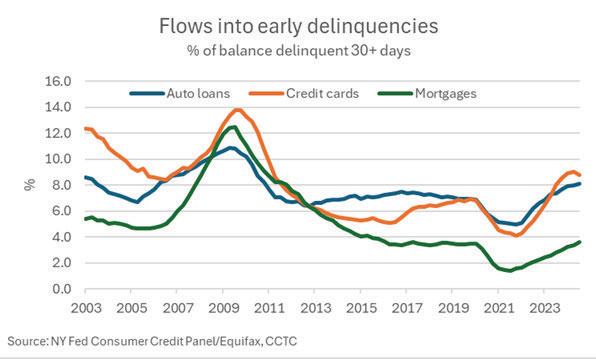

Early delinquencies, particularly those transitioning into more serious delinquencies (30+ days) indicate potential financial distress among borrowers. Recent data shows worrisome trends for both auto loans and credit cards and should be monitored closely. Auto loans delinquent 30+ days have reached levels last seen in Q4, 2010. Similarly, credit card delinquencies of 30+ days are at the highest level since Q1, 2011. Again, the lower income borrower is in focus.

Early delinquencies, particularly those transitioning into more serious delinquencies (30+ days) indicate potential financial distress among borrowers. Recent data shows worrisome trends for both auto loans and credit cards and should be monitored closely. Auto loans delinquent 30+ days have reached levels last seen in Q4, 2010. Similarly, credit card delinquencies of 30+ days are at the highest level since Q1, 2011. Again, the lower income borrower is in focus.

Market Multiples and Concentration

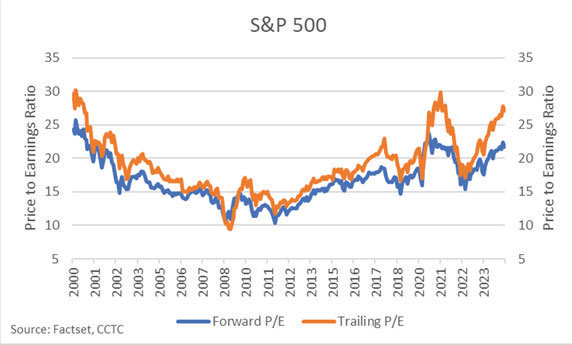

One metric commonly used to judge whether a stock (market) is valued appropriately is the Price-to-Earnings (P/E) ratio. A high P/E ratio may indicate that a stock (market) is overvalued while a low P/E ratio might suggest it is undervalued. The S&P 500 currently trades at a forward P/E ratio of 21.5X and trailing P/E ratio of 27X. The forward P/E ratio is telling us that the S&P 500 is valued at 21.5X consensus earnings forecast over the next 12 months. The trailing P/E ratio shows the index’s value given trailing 12-months earnings. While the forward multiple could be deceiving, given that forward earnings estimates could be low, the trailing multiple is less likely to be misleading given past earnings are known. By the trailing P/E ratio metric alone, the S&P 500 could look expensive.

One metric commonly used to judge whether a stock (market) is valued appropriately is the Price-to-Earnings (P/E) ratio. A high P/E ratio may indicate that a stock (market) is overvalued while a low P/E ratio might suggest it is undervalued. The S&P 500 currently trades at a forward P/E ratio of 21.5X and trailing P/E ratio of 27X. The forward P/E ratio is telling us that the S&P 500 is valued at 21.5X consensus earnings forecast over the next 12 months. The trailing P/E ratio shows the index’s value given trailing 12-months earnings. While the forward multiple could be deceiving, given that forward earnings estimates could be low, the trailing multiple is less likely to be misleading given past earnings are known. By the trailing P/E ratio metric alone, the S&P 500 could look expensive.

We can explain this by the large-cap growth names that dominate the market-weight of the S&P 500 index. The top 10 stocks by weighting (all technology related except Berkshire Hathaway) account for 37% of the total market-capitalization of the S&P index and have an average forward P/E of 29.5X. The S&P 500 is a market index where each component’s weight is determined by its total market capitalization, calculated as the stock price multiplied by the number of outstanding shares. This means that larger companies have a greater influence on the index’s performance than smaller companies.

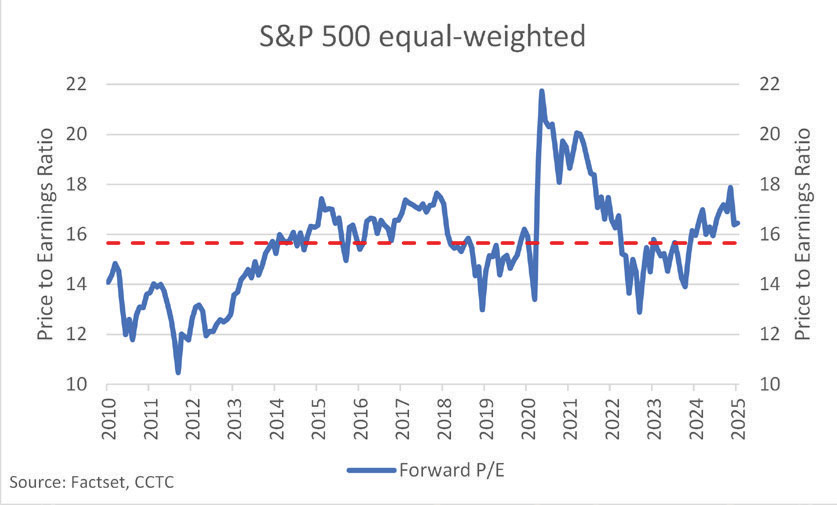

However, as we have shown in the past, the average stock in the S&P 500 does not look as expensive as the trailing P/E ratio might otherwise indicate. When we equal-weight stocks in the index, where smaller companies have an equivalent effect on the index as larger companies, the index is trading just above its 25-year median value. It’s not necessarily true that the explosive growth in value of many large-cap technology related companies isn’t warranted; it may be. However, we believe that excessive optimism may be occurring in parts of the market, and we are focused on controlling risk. One particular risk we are watching is the 10-year U.S. Treasury yield. In the past, a yield of around 5% or above has been negative to high flying technology names.

However, as we have shown in the past, the average stock in the S&P 500 does not look as expensive as the trailing P/E ratio might otherwise indicate. When we equal-weight stocks in the index, where smaller companies have an equivalent effect on the index as larger companies, the index is trading just above its 25-year median value. It’s not necessarily true that the explosive growth in value of many large-cap technology related companies isn’t warranted; it may be. However, we believe that excessive optimism may be occurring in parts of the market, and we are focused on controlling risk. One particular risk we are watching is the 10-year U.S. Treasury yield. In the past, a yield of around 5% or above has been negative to high flying technology names.

Our portfolios are managed with both your risk tolerance and return objective in mind. We genuinely believe that time in the market is key, as attempting to time the market is a fool’s errand. In our view, compounding returns of high-quality portfolios is key towards achieving your financial goals.

All of us at Country Club Trust Company, along with the entire Country Club Bank organization, hope that you and your families are well. Please be assured that we continue to work diligently on your behalf, providing the level of service you have come to expect and deserve. As always, we are ready and willing to be of assistance in any way we can. Should you have any questions, we are always here for you.

Take care.