A View from the Tower – Second Quarter 2024

Déjà Vu All Over Again

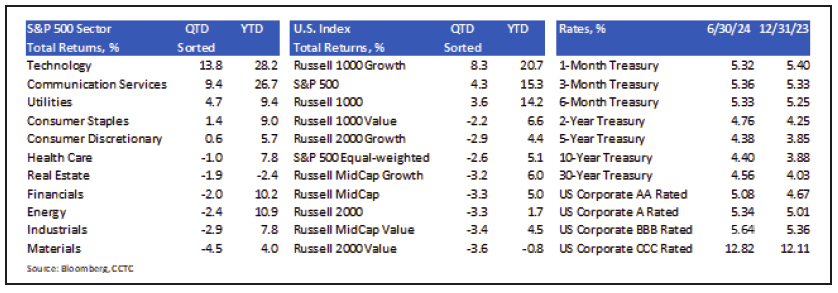

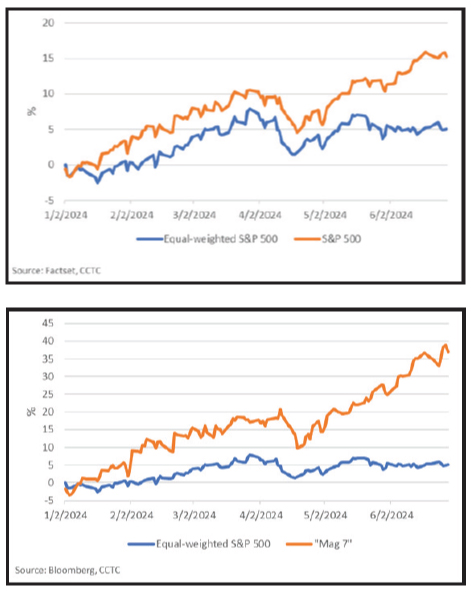

The second quarter of 2024 brought early jitters to equity market investors before finishing on solid ground. On a total return basis, the S&P 500 rose 4.3%, reaching a record high nine times during the period. For the year, the index is up 15.3%; 5.1% equal weighted. As has been the theme since the beginning of 2023, the strong Q2 performance was driven by surging semiconductor stocks and tech mega-caps, even though most of the index declined. Only three sectors of the S&P 500 index had considerable gains during the quarter: technology, communication services and utilities. Notably, the artificial intelligence (AI) theme extended beyond technology, with utilities stocks also benefiting as Wall Street considered the AI revolution’s electricity needs. However, some market participants expressed concern about the rally being driven by a limited number of stocks and high index concentration in technology related names such as the “Magnificent 7”, or “Mag 7.”

The second quarter of 2024 brought early jitters to equity market investors before finishing on solid ground. On a total return basis, the S&P 500 rose 4.3%, reaching a record high nine times during the period. For the year, the index is up 15.3%; 5.1% equal weighted. As has been the theme since the beginning of 2023, the strong Q2 performance was driven by surging semiconductor stocks and tech mega-caps, even though most of the index declined. Only three sectors of the S&P 500 index had considerable gains during the quarter: technology, communication services and utilities. Notably, the artificial intelligence (AI) theme extended beyond technology, with utilities stocks also benefiting as Wall Street considered the AI revolution’s electricity needs. However, some market participants expressed concern about the rally being driven by a limited number of stocks and high index concentration in technology related names such as the “Magnificent 7”, or “Mag 7.”

The “Mag 7” (Microsoft, Amazon, Meta, Apple, Alphabet, Nvidia and Tesla) currently account for approximately 33% of the market-weighted S&P 500 index. Obviously, the performance of these equities has a considerable influence on the index. The average stock was down by 2.6% in Q2, while the “Mag 7” was up 16.9%. In the most recent quarter, this small group of stocks accounted for 112% of the S&P 500 return. Year-to-date they accounted for 59% of the return.

An Inflation Scare Provided a Rough Start to Q2

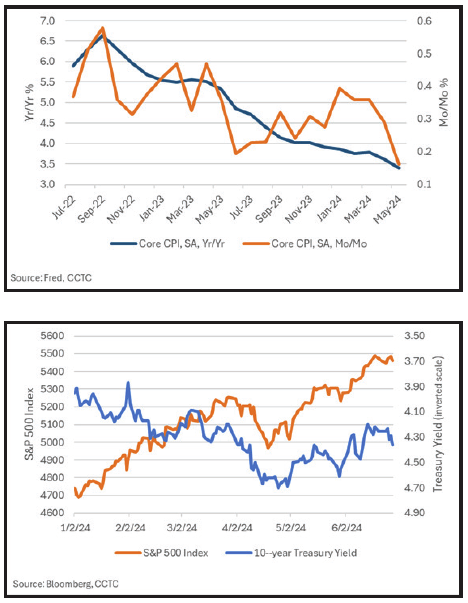

On a year-over-year basis, we have made substantial progress on inflation since its peak in September of 2022. However, we did see a little bit of a stall in our inflation fight beginning in the summer of 2023. The Core Consumer Price Index (Core CPI) began rising on a month- over- month basis. The six to seven interest rate cuts initially projected for 2024 were gradually shunned. As a result, longer-term Treasury yields began rising.

On a year-over-year basis, we have made substantial progress on inflation since its peak in September of 2022. However, we did see a little bit of a stall in our inflation fight beginning in the summer of 2023. The Core Consumer Price Index (Core CPI) began rising on a month- over- month basis. The six to seven interest rate cuts initially projected for 2024 were gradually shunned. As a result, longer-term Treasury yields began rising.

Eventually, inflation readings once again trended in a favorable direction. We believe much of the market action in 2024 can be explained by looking at Treasury yields (in addition to corporate earnings) versus the S&P 500, recognizing that the “Mag 7” stocks are long duration assets with a significant degree of sensitivity to changes in interest rates. As the 10-year Treasury yield continued to rise through the spring, a minor correction occurred in the technology heavy S&P 500. As yields subsequently retreated, the “Mag 7,” and therefore the S&P 500, recovered to all-time highs.

We Believe the Economy Continues to Slow

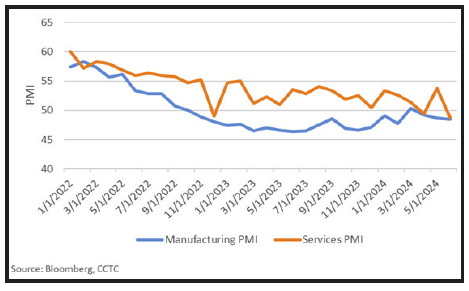

The Manufacturing Purchasing Managers’ Index (PMI) and Services PMI Index are crucial economic indicators that gauge prevailing trends in the manufacturing and services sectors. It is difficult to find real-time economic data that is a better indicator of the U.S. economy’s performance. These PMI’s combine indices for new orders, output, employment, suppliers’ delivery times and inventory levels. Readings below 50 suggest a contraction in business activity from the prior month, while readings above 50 suggest an expansion. The manufacturing PMI suggests the manufacturing sector has been in a contraction since November of 2022, with index readings below 50 for nineteen out of the last twenty months. However, the services sector, which represents about 80% of our economy, has seemingly been holding up well enough to keep the economy humming along. However, this appears to be changing potentially, as the Services PMI posted in June its second contractionary month in four.

The Manufacturing Purchasing Managers’ Index (PMI) and Services PMI Index are crucial economic indicators that gauge prevailing trends in the manufacturing and services sectors. It is difficult to find real-time economic data that is a better indicator of the U.S. economy’s performance. These PMI’s combine indices for new orders, output, employment, suppliers’ delivery times and inventory levels. Readings below 50 suggest a contraction in business activity from the prior month, while readings above 50 suggest an expansion. The manufacturing PMI suggests the manufacturing sector has been in a contraction since November of 2022, with index readings below 50 for nineteen out of the last twenty months. However, the services sector, which represents about 80% of our economy, has seemingly been holding up well enough to keep the economy humming along. However, this appears to be changing potentially, as the Services PMI posted in June its second contractionary month in four.

Labor Market Finally Normalizing

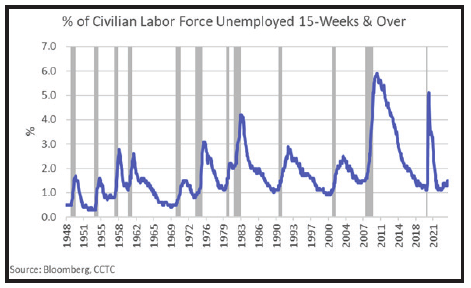

After bottoming in April of 2023 at 3.4%, the unemployment rate has begun to tick higher over the past year. The last reading of 4.1% surprised market forecasters, and we might see more surprises ahead. The percent of the labor force unemployed for 15-weeks and over has been a good leading indicator of the unemployment rate in the past. For sure, the unemployment rate is a lagging indicator of the overall economy’s health. But, in our view, a little bit of slack in the labor force, along with continued moderation of inflation, is what the Fed has been waiting for before cutting interest rates. The Fed and the market may finally be getting on the same page this cycle. The market is expecting two rate cuts this year, the first in September.

After bottoming in April of 2023 at 3.4%, the unemployment rate has begun to tick higher over the past year. The last reading of 4.1% surprised market forecasters, and we might see more surprises ahead. The percent of the labor force unemployed for 15-weeks and over has been a good leading indicator of the unemployment rate in the past. For sure, the unemployment rate is a lagging indicator of the overall economy’s health. But, in our view, a little bit of slack in the labor force, along with continued moderation of inflation, is what the Fed has been waiting for before cutting interest rates. The Fed and the market may finally be getting on the same page this cycle. The market is expecting two rate cuts this year, the first in September.

Do not Count Out Equity Markets in an Election Year

Although we may finally be seeing the economy slowing, with falling inflation and higher unemployment, we cannot assume it will continue into the fall. Spending associated with the Infrastructure Investment and Jobs Act, passed in 2021, should ramp-up into the elections. Incumbent parties do not like to lose when running for a second Presidential term and at this point the election seems like it could be historically tight. Greasing the wheels in an election year is commonplace. Equities typically enjoy the ride.

Our portfolios are managed with both your risk tolerance and return objective in mind. We genuinely believe that time in the market is key, as attempting to time the market is a fool’s errand. In our view, compounding returns of high-quality portfolios is key towards achieving your financial goals.

All of us at Country Club Trust Company, along with the entire Country Club Bank organization, hope that you and your families are well. Please be assured that we continue to work diligently on your behalf, providing the level of service you have come to expect and deserve. As always, we are ready and willing to be of assistance in any way we can. Should you have any questions, we are always here for you.

Take care.