Why We are Optimistic for M&A in 2024

Following the red-hot M&A market that came on the heels of Covid-19, momentum swung sharply in 2023 as economic uncertainty and high interest rates took a toll on deal volume and valuations. A new year brings with it an evolving deal environment that we expect to become more positive as 2024 progresses. Here are a few reasons for optimism in 2024:

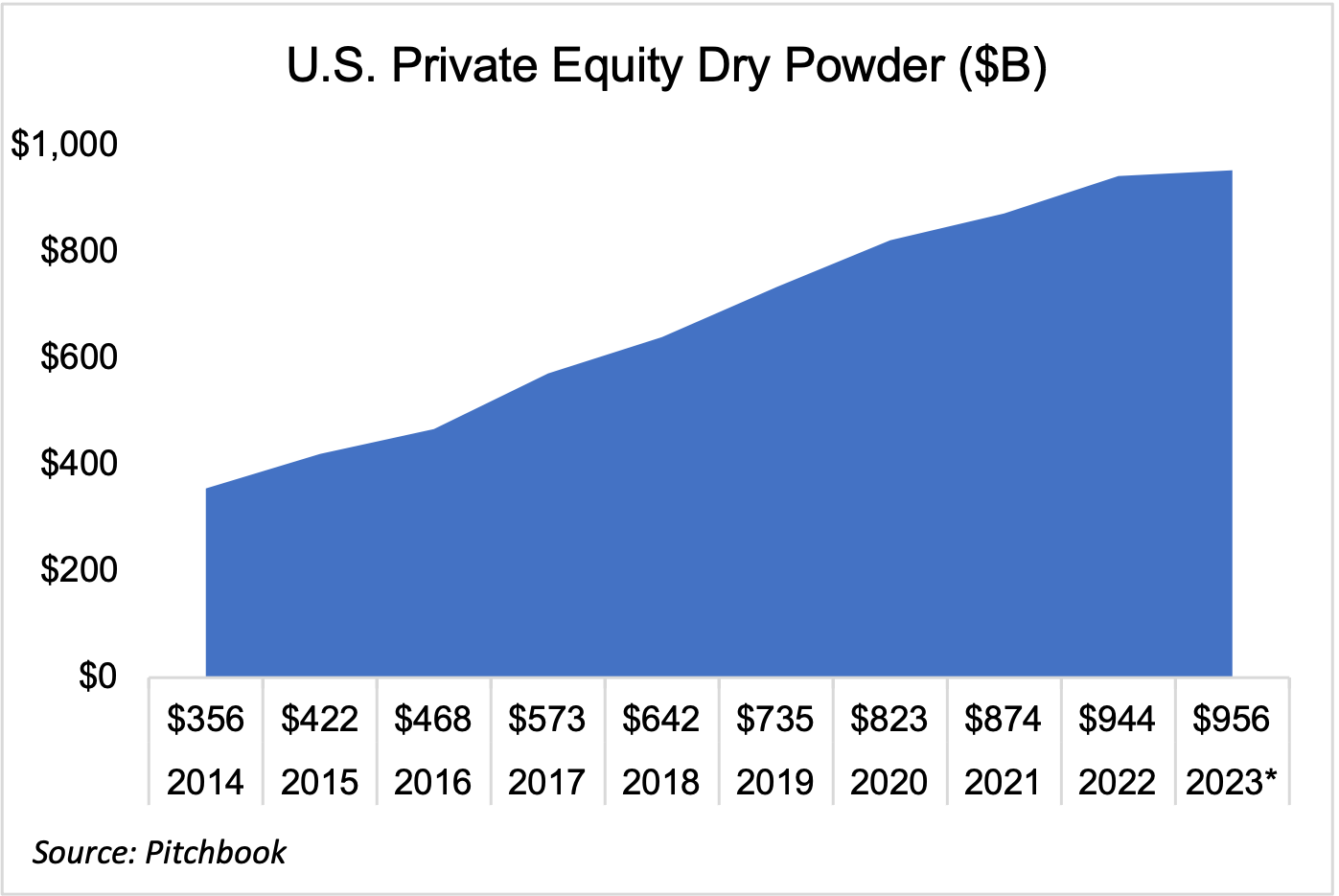

Record Dry Powder

Record Dry Powder

We may sound like a broken record, but once again U.S. private equity dry powder (the capital a firm has available to make acquisitions) hit a record high in 2023 for the ninth year running. While firms focused more on smaller add-on acquisitions than larger platforms due to a tough lending environment (more on that below), fundraising continued resulting in over $955 billion of dry powder. We expect firms will continue to seek add-on acquisitions in 2024 but will also selectively pursue larger platforms in order to deploy more capital.

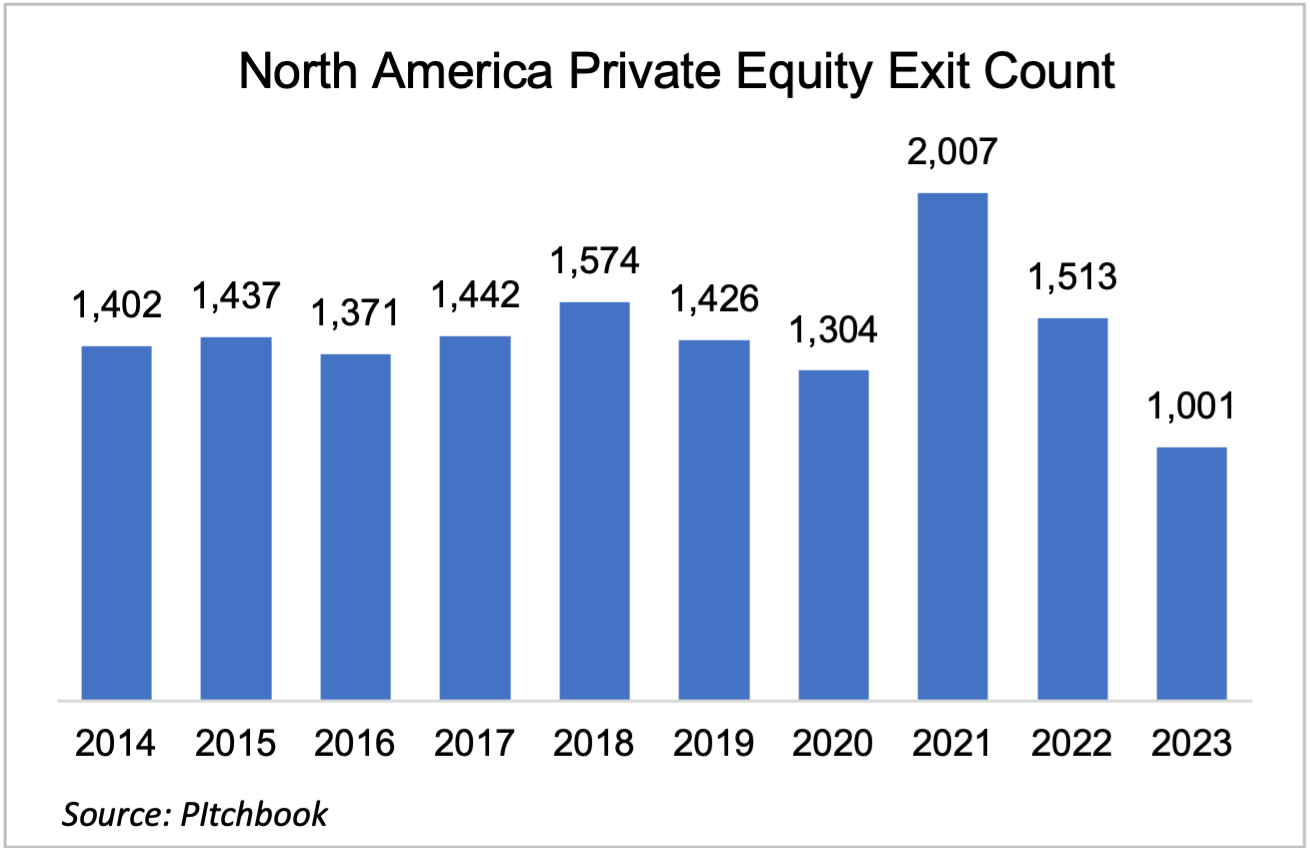

As greater emphasis is placed on large deals, we expect private equity firms will opportunistically begin selling portfolio companies that have been held for longer periods to generate returns for investors. According to Pitchbook, in 2023, private equity’s exit count hit a 13-year low and the median holding period of U.S. private equity investments exited was 6.4 years, a peak since 2015. Private equity investors have the luxury of being able to wait out the market until conditions improve.  As the IPO market comes back to life and strategic and financial buyers alike begin to pursue acquisitions of all sizes more aggressively, more exit opportunities will be available, and private equity firms will become sellers in 2024. We expect private equity exits to pick up, particularly in the lower middle market where sponsor-to-sponsor transactions are more prevalent.

As the IPO market comes back to life and strategic and financial buyers alike begin to pursue acquisitions of all sizes more aggressively, more exit opportunities will be available, and private equity firms will become sellers in 2024. We expect private equity exits to pick up, particularly in the lower middle market where sponsor-to-sponsor transactions are more prevalent.

Expected Interest Rate Cuts

High interest rates were a drag on valuations in 2023, as buyers relied more heavily on equity than debt in transaction structures and banks got more stringent with lending standards. In December, the Fed indicated that the interest rate hikes, that had begun in early 2022 and continued through 2023, had been successful in driving down inflation and rates were “at or near” a peak. Now analysts are speculating that rate cuts will likely begin in the second quarter of 2024 with 3-4 additional cuts by year- end, an expectation that is welcome news for the M&A market. While borrowing costs will still be relatively high and lenders are expected to be selective with opportunities, buyers will find creative ways to structure deals to minimize cash at close. Sellers may find it advantageous to provide seller financing at high-interest rates to bridge the gap.

Valuations Reach Consensus

A prevalent challenge in today’s market is a mismatch of valuation expectations between buyers and sellers. For buyers, increased borrowing costs have driven valuations lower, but sellers with fundamentally strong and growing companies expect valuations in line with those achieved in 2021 and 2022 when M&A was at its peak. We predict sellers will take a more reasonable stance in 2024, while buyers will use the advantage of a falling interest rate environment to increase valuation, particularly in competitive processes. Overall, we expect valuations to trend slightly higher in 2024, which will generate more deal flow.

There will undoubtedly be unexpected events that may be to the benefit or detriment of M&A transactions throughout 2024, but fundamentally we believe the biggest factor will be the need to deploy significant cash, which will drive M&A activity and valuations up. Market timing can be difficult to navigate for a business owner who is ready to exit, so we recommend finding a trusted and qualified advisor to guide through the decision of when and how to best approach a sell-side transaction.